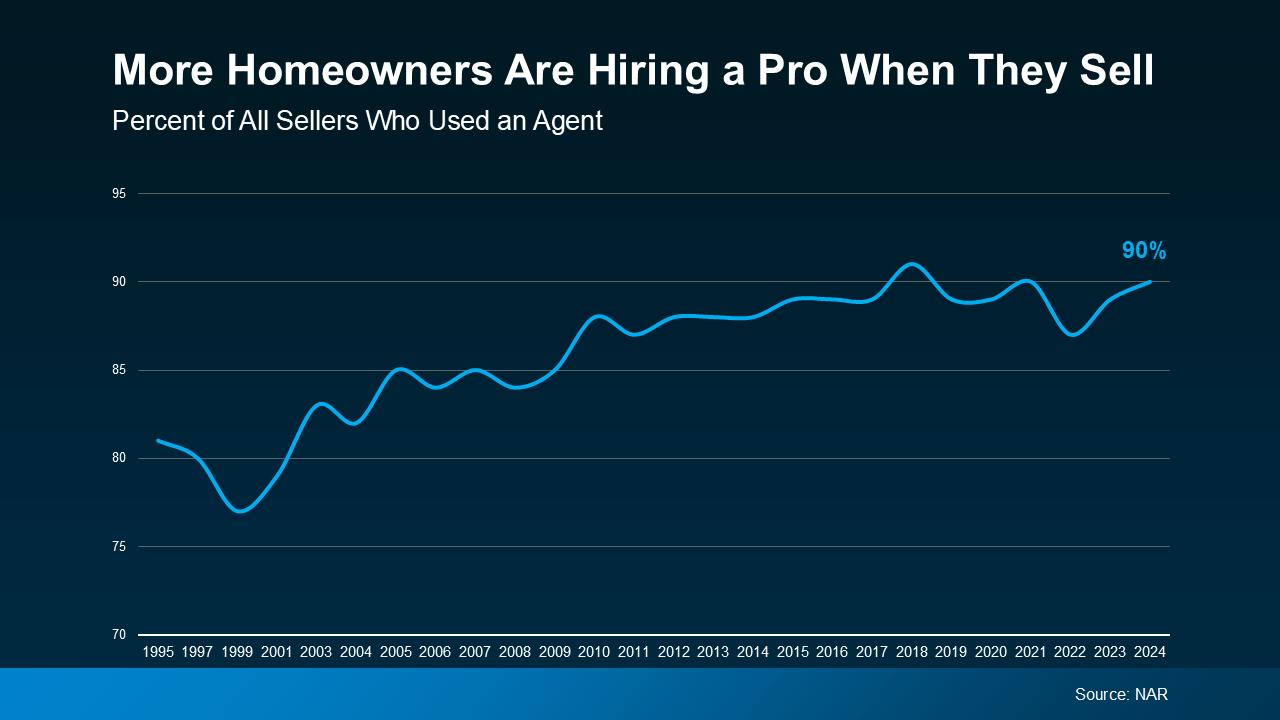

The Top 2 Reasons To Look at Newly Built Homes

When planning a move, a newly built home might not be the first thing that comes to mind. But with more brand-new homes on the market and builders focusing on smaller, more affordable options, this type of home may just be the key to crossing the homebuying finish line.

Here’s why a new build is worth considering – and how an agent can help you find one that meets your needs and your budget.

1. More Newly Built Homes Are Available Right Now

First, let’s break down the types of homes on the market. A newly built home is a house that was just built or is under construction. On the other hand, an existing home is one a homeowner has already lived in.

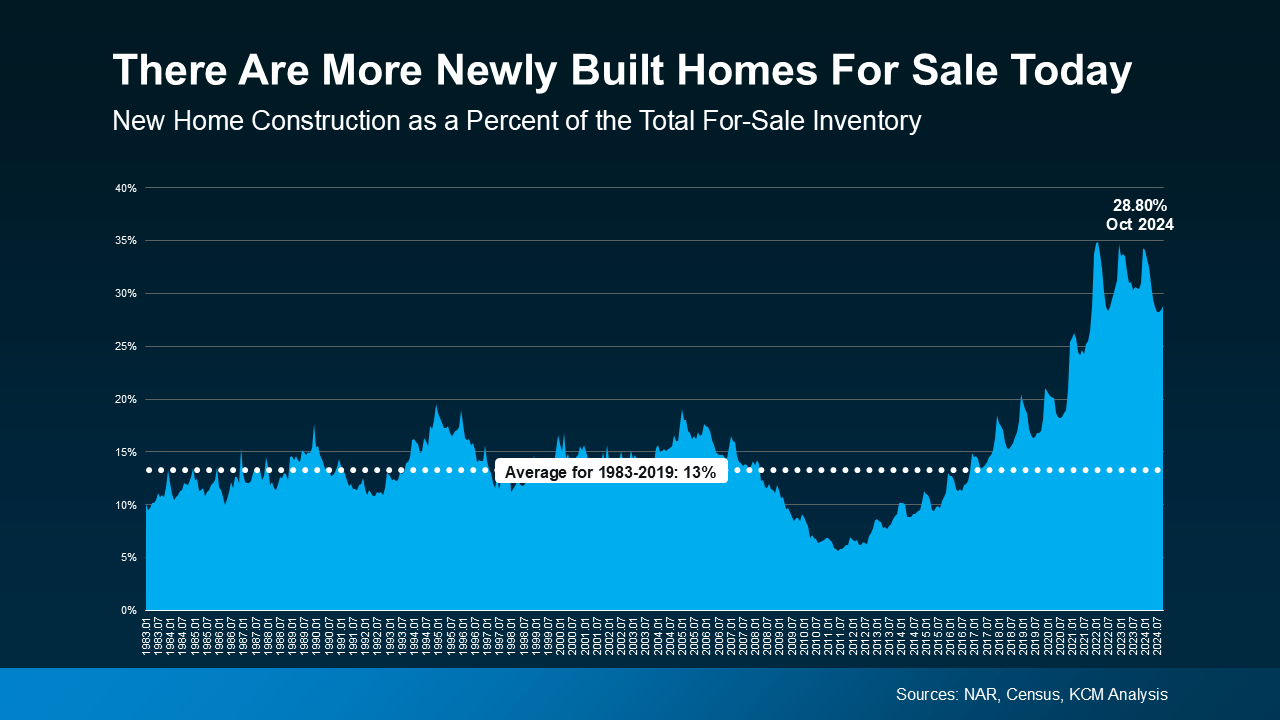

Right now, the number of existing homes for sale is still low. And, if you’re struggling to find something you like because there aren’t that many existing homes for sale, opening up your search to include brand-new homes could really expand your options. That’s because there are more newly built homes available right now than in a typical year (see graph below):

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“Even though existing home sales have been stuck at low levels, newly constructed home sales look to mark one of its best annual performance in 15 years . . . The new home inventory has been consistently rising with homebuilders getting active and making up around 1/3 of total inventory.”

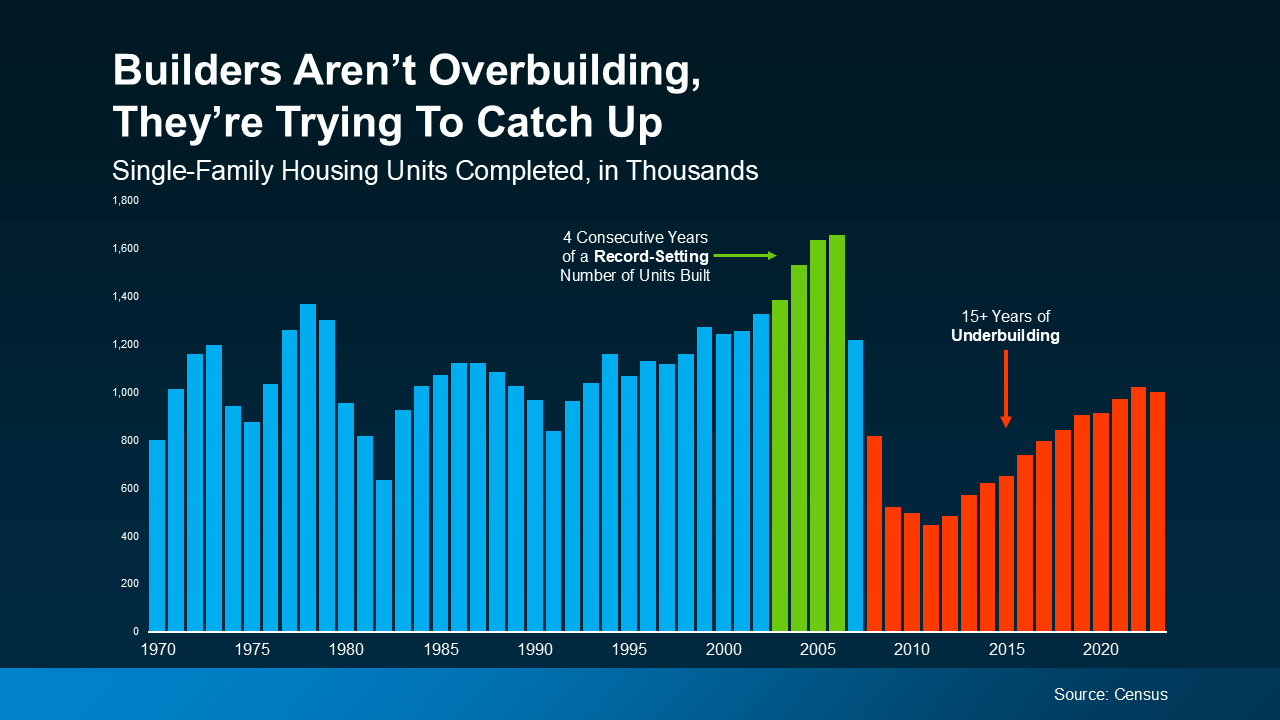

While the uptick in new home construction is encouraging, rest assured that builders aren’t overdoing it, they’re just making up for over a decade of underbuilding. There are still way more buyers than there are homes on the market. But the good news for you is this increase in newly built homes means more options for your search.

2. Newly Built Homes Are Becoming Less Expensive

Still skeptical if a new build is right for you or if they’re even in your budget? The average cost of newly built homes has actually come down from a year ago.

Why is that? Builders know affordability is top of mind for homebuyers right now. So they’re focusing their efforts on building smaller homes they can offer at lower price points and are more likely to sell. As Realtor.com says:

“Builders are increasingly bringing smaller, more affordable homes to the market, so buyers may find more newly-built homes that fit their budget.”

Something to keep in mind: buying a newly built home isn’t the same as buying an existing one. Builder contracts have different fine print. So be sure to partner with a local agent who knows the market, builder reputations, and what to look for in those contracts.

Bottom Line

Depending on your needs and budget, a new build might be the opportunity you’ve been waiting for to bring your homebuying vision to life. If you’re interested in a brand-new home, connect with an agent so you can check out what builders in your area are up to.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.