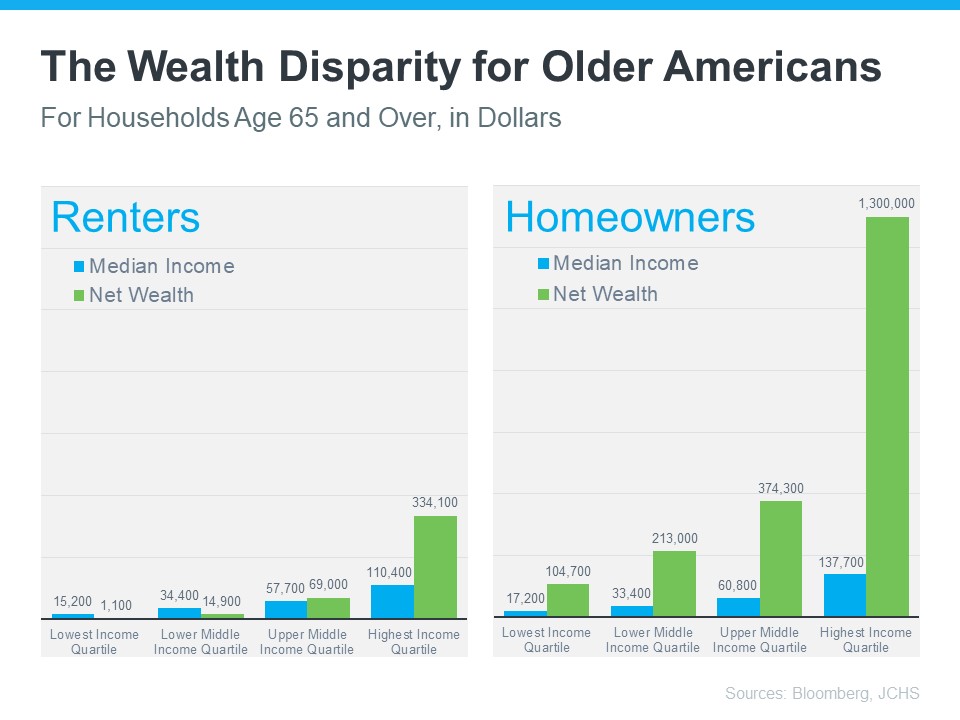

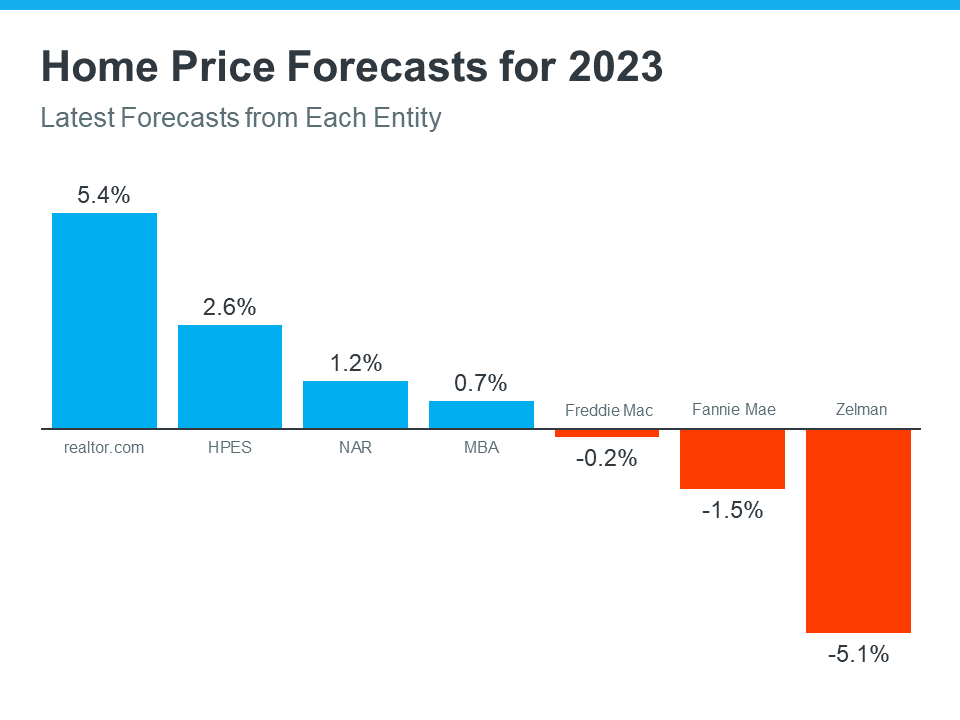

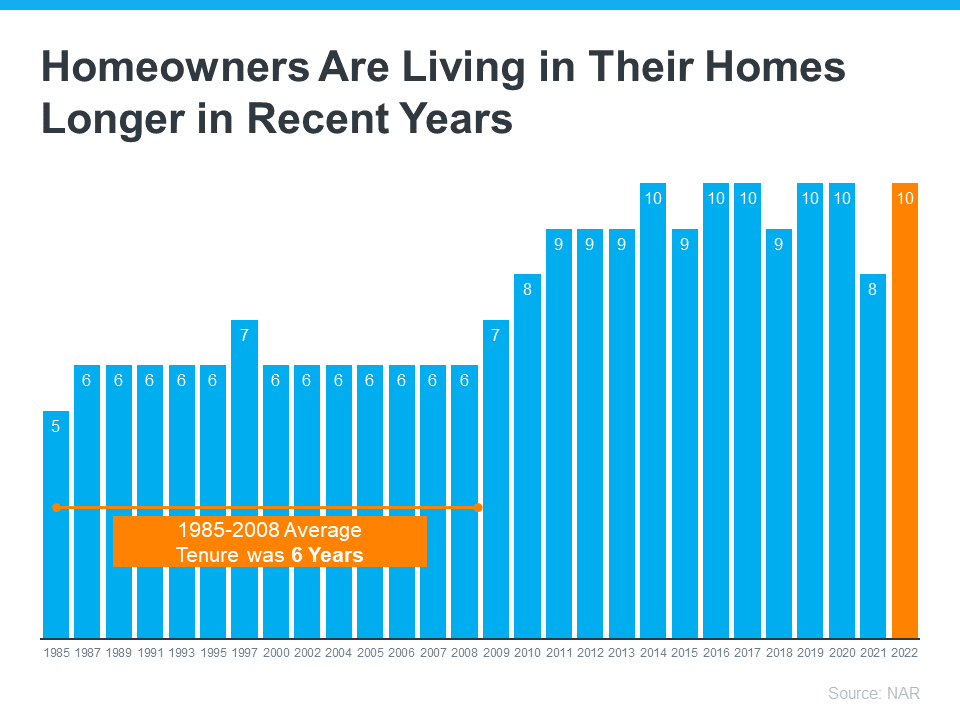

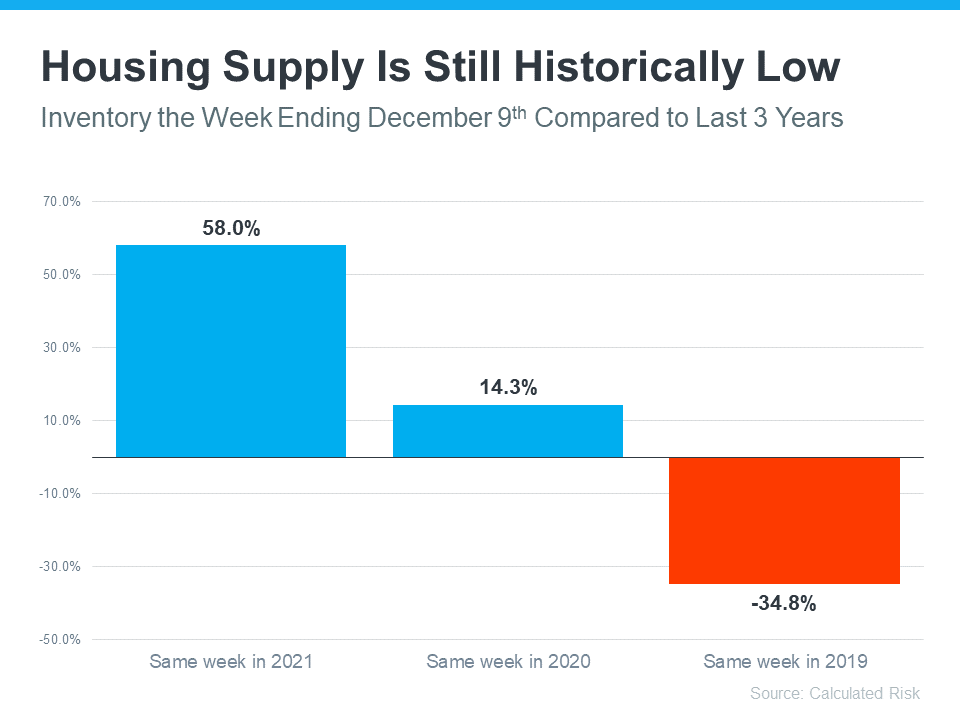

2023 Housing Market Forecast [INFOGRAPHIC]

![2023 Housing Market Forecast [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/12/15124934/2023-Housing-Market-Forecast-KCM-Share-549x300.png)

![2023 Housing Market Forecast [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/12/15124929/2023-Housing-Market-Forecast-MEM.png)

Some Highlights

- From home sales to prices, the 2023 housing market will be defined by mortgage rates. And where rates go depends on what happens with inflation.

- If you’re thinking of buying or selling a home this year, let’s connect so you understand where the housing market is headed in 2023.

Sources:

- realtor.com

- Home Price Expectations Survey (HPES)

- National Association of Realtors (NAR)

- Mortgage Bankers Association (MBA)

- Fannie Mae

- Freddie Mac

- Zelman & Associates

- Greg McBride, Chief Financial Analyst, Bankrate

Content previously posted on Keeping Current Matters

![Reasons To Sell Your House This Season [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/12/08120834/Reasons-To-Sell-Your-House-This-Season-KCM-Share-549x300.png)

![Reasons To Sell Your House This Season [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/12/08120835/Reasons-To-Sell-Your-House-This-Season-MEM.png)