3 Hot Topics in the Housing Market Right Now

If you’re a prospective buyer or seller, it’s important to understand the current real estate market conditions and how they affect you. The Counselors of Real Estate (CRE) just released its Top Ten Issues Affecting Real Estate report. Here are three hot topics from the list and how they impact today’s housing market.

Technology Acceleration and Innovation

The past year ushered in many changes to the real estate industry, especially when it comes to technology. The CRE report elaborates on this:

“Lockdown-driven changes in our work, in the economy, in social structures, and in our personal behavior have pushed our reluctance aside. The acceleration and adoption of technology during the pandemic has impacted everything, and real estate is no exception.”

For real estate, innovations like digital documentation, virtual tours, and video chat enable agents to connect with clients no matter their location. These options are ideal for prospective buyers and sellers who aren’t local to the area or those that need the added flexibility signing documents online or doing virtual tours provide. That’s why many trusted real estate advisors will continue to use these technologies moving forward to best serve their clients.

Remote Work and Mobility

Working from home became the reality for many individuals during the pandemic, and the latest list from the CRE identified remote work and mobility as an important influence on the real estate market. As the report notes:

“…the pandemic universally caused a movement away from urban cores, particularly for those with higher incomes who could afford to move and for lower-income individuals seeking lower costs of living. Most of these relocations remained within their original region—84%—and, while some are returning, it is unknown as to the permanence of these movements or whether they represent a true urban exodus.”

With the added mobility remote work offers, where people are moving and where they can ultimately purchase a home is less dependent on a physical office location. This newfound flexibility is giving remote workers the opportunity to move to more affordable areas and buy more home for their money.

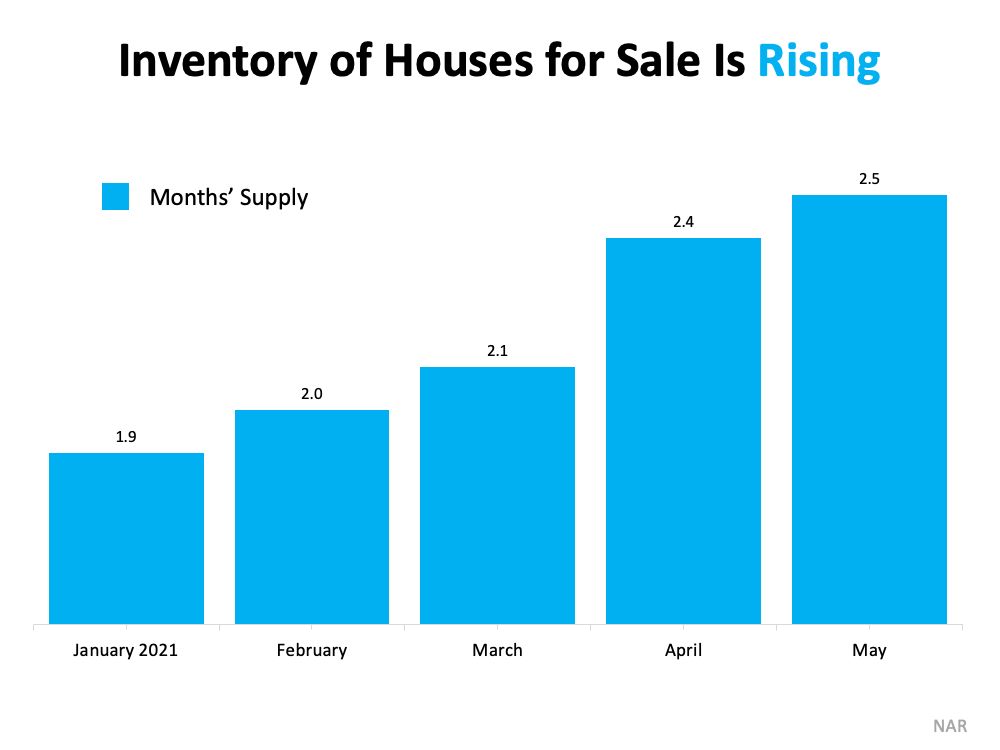

Housing Supply and Affordability

Finally, the limited supply of houses for sale and the related affordability challenges also makes CRE’s list of key factors this year:

“According to the National Association of Realtors®, the state of America’s housing inventory is dire, with a chronic shortage of affordable and available homes needed to support the nation’s population.”

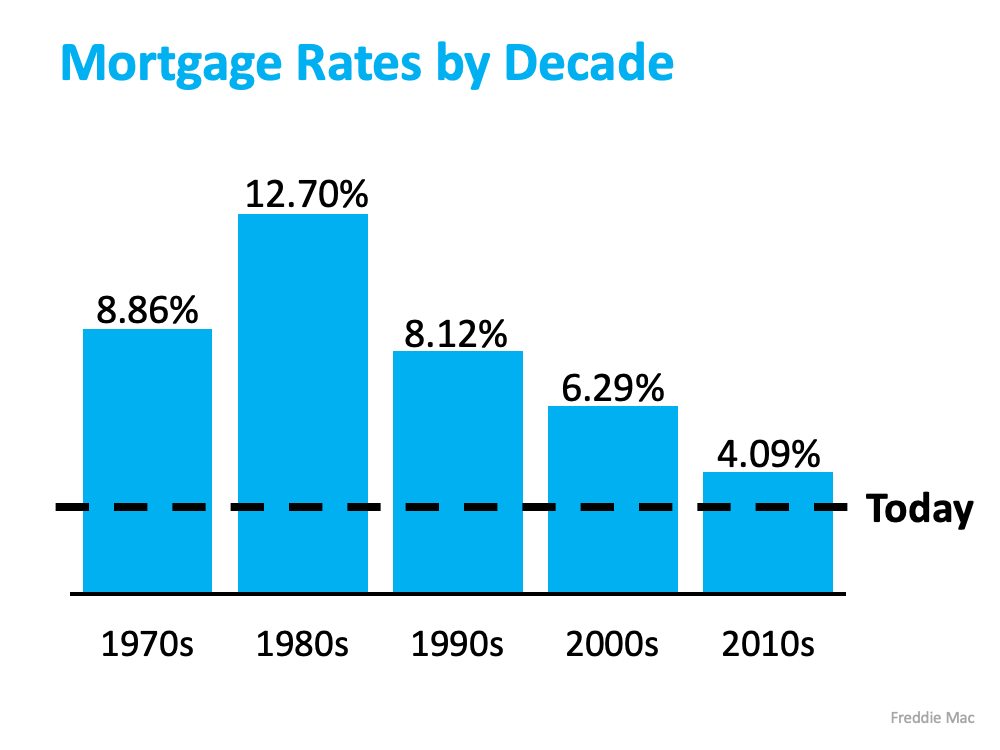

There is good news. Homes are still more affordable than they have been historically thanks to today’s low mortgage rates. And while housing supply is still low, we’re seeing steady increases in the number of homes coming to market, which gives hope to homebuyers. As the supply of homes for sale improves, buyers will have more options.

Bottom Line

New technology, remote work, housing supply, and home affordability are key factors in the housing market right now for both buyers and sellers. If you want to better understand how these topics can impact you, let’s connect today.

Content previously posted on Keeping Current Matters

![Pop Quiz: Can You Define These Key Terms in Today’s Housing Market? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/22135655/20210723-KCM-Share-549x300.png)

![Pop Quiz: Can You Define These Key Terms in Today’s Housing Market? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/22135657/20210723-MEM.png)

![Experts Agree: Options Are Improving for Buyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/15150310/20210716-KCM-Share-549x300.png)

![Experts Agree: Options Are Improving for Buyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/15150312/20210716-MEM.png)